July 19 2023 - 6:00pm

Recent reports suggest that gilts, or British Government bonds, are becoming increasingly hard to sell. The main reason for this is that investors see British inflation as much more stubborn than elsewhere in the world, and so expect that the Bank of England will have to raise interest rates higher, therefore making holding gilts more risky.

British Government bond yields are now substantially higher than yields on American equivalents, and far higher than European yields. One hedge fund manager recently told me that traders are comparing the gilt market to a government bond market in a developing country.

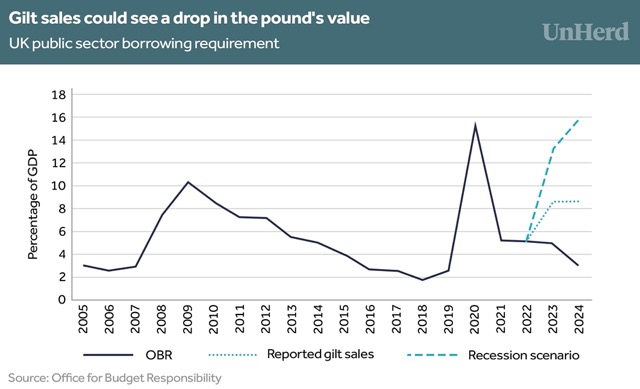

These developments could not have come at a worse time. The Government is preparing to sell £241 billion worth of gilts in the current fiscal year, over £100 billion more than it issued last year. If these reports are accurate, the Government’s fiscal deficit — or “public sector borrowing requirement” (PSBR) — will be far higher than currently being projected.

The Office for Budget Responsibility (OBR), which independently forecasts the economy and public borrowing, puts the PSBR at around 5.1% of GDP in 2022-23. But if we take the £241 billion worth of bonds reportedly issued this fiscal year and plug in the OBR’s own growth and inflation projections, we get a PSBR of around 8.6% of GDP. This is an unprecedented level of public borrowing outside a recession.

Things look even worse when factoring in the possibility of a recession. House prices are currently contracting, with data from property-listing websites like Rightmove showing a decline in asking prices. This raises the possibility that we get a repeat of the 2008-09 recession, which was the last time the property market sagged to this extent and when layoffs started in the construction sector.

Taking the reported £241 billion number and then modelling a recession driven by a burst property bubble shows that public borrowing tops out at an eye-watering 13.1-15.8%. While there were similar levels of borrowing during 2020 because of the lockdown, this was generally attributed to exceptional circumstances. Yet these numbers suggest that the borrowing in 2020 could easily be repeated in the near future without the need for lockdowns.

What does this mean for the British economy? Unlike in other developed countries, Britain’s currency is very sensitive to fluctuations in capital movements. If the economy were to enter a recession and the Government forced to sell huge amounts of gilts in a market that is not particularly keen to buy them, sterling could well fall in value.

Indeed, the last recession instigated a decline in currency, with sterling falling by around 20% against the US dollar and never really recovering. A fall in sterling would mean an increase in import prices, and since approximately one in three goods consumed in Britain is imported, this would mean more inflationary pressure. Hard times lie ahead for the UK’s economy.

Philip Pilkington is a macroeconomist and investment professional, and the author of The Reformation in Economics

philippilk

philippilk