March 24 2021 - 11:51am

‘Margin debt’ is an inconspicuous name for a potentially explosive issue. It’s the jargon for borrowing from a stock broker to buy shares. Instead of using money you’ve already got to fund the whole of the purchase, you buy a proportion of the shares on tick.

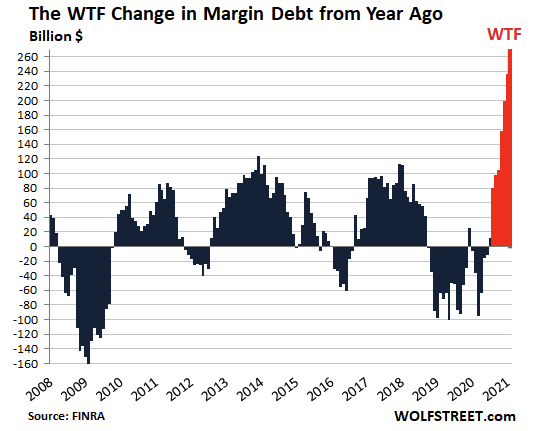

It’s a long established practice, but during the pandemic, margin debt has gone through the roof. In America, some financial analysts are beginning to sound the alarm. For instance, see this chart from the Wolf Street blog, which shows the ups and downs in margin debt levels since the global financial crisis of 2008:

As you can see, the last year or so looks intensely spiky. Or as the author, Wolf Richter, puts it: “the zoo has gone nuts.”

Certainly it helps to explain why share prices have recovered so well following their precipitous fall at the beginning of the Covid crisis. Once it became clear that western governments would borrow and print to keep their economies afloat, investors regained their confidence. Indeed, they began to salivate at the prospect of what all that economic stimulus was going to do to artificially inflate asset prices.

So no wonder investors have piled back into shares — if necessary borrowing the money to maximise their purchases.

Arguably this has been a good thing — at least in the short-term. If stock markets and property markets had crashed without recovering, the whole world could have tipped over into Covid-fuelled economic depression.

But as we vaccinate and unlock our way back to recovery, there’s a danger of unleashing an unsustainable boom, followed by a post-stimulus slump. Debt has a habit of exaggerating both the highs and the lows. Debt used to buy shares is especially risky. Obviously it helps to pump money into overheating markets, but when bubbles burst it also helps to accelerate the bust. That’s because when share prices are falling, brokers demand more cash from, and extend less credit to, their clients — who then get hold the cash by selling shares, thereby further reducing prices.

What can governments do to keep things under control? Well aside from maintaining the stabilisation mechanisms put in place after the global financial crisis, they need to send a long-term signal to the markets that real investment in actually productive economic activity is going to be consistently favoured over financial engineering.

It’s not that pure speculation ought to be banned, because as long as markets exist, they’ll always find a way. However, the windfall profits of such activity can and should be taxed more heavily — and revenues used to support the long-term investment and innovation that we need now more than ever.