January 14 2021 - 12:06pm

Every saver knows that interest rates are freakishly low. In fact, they’ve been on the floor for more than a decade now. But is this just a weird anomaly?

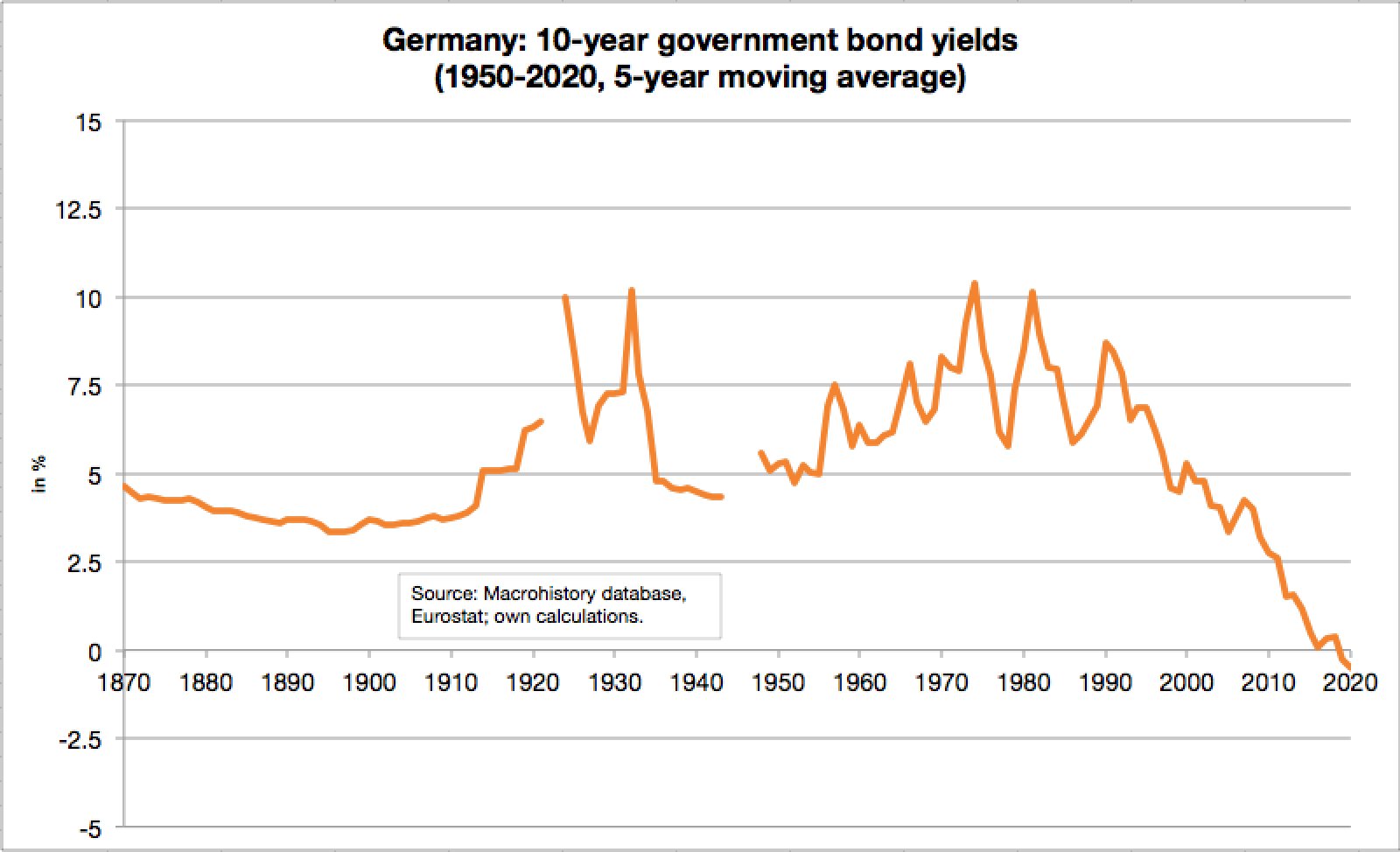

A chart tweeted out today by the economist Philipp Heimberger would suggest not. It shows the long-term trend in German interest rates (on government debt) over the last 150 years:

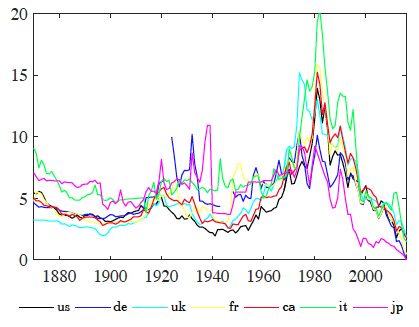

The most important trend is the remarkably steady fall over the last 30 years. Much the same has happened in all the G7 economies — as the following chart shows:

It’s tempting to blame this phenomenon on the series of unfortunate events that began with the banking crisis of 2008. But it’s now plain to see that the long collapse of interest rates started well before any of that.

The global disruption caused by the pandemic is the final test. If there’s no return to inflation (plus interest rate rises) then we’ll need to accept that we’ve entered a new era — one with permanently low rates.

This will have profound consequences. In fact, we’re already seeing signs of a shockingly new economic order. For instance, in Denmark, borrowers can now get a zero per cent mortgage. Just to be clear, this doesn’t mean a no deposit mortgage, it means that the borrower pays zero per cent interest. Furthermore, that’s fixed for 20 years — which demonstrates a sincere belief on the part of the lender that the new normal is here to stay.

A few years ago, Danish government was one of the first to get away with borrowing from the markets at zero per cent interest — now ordinary Danes can do the same. Of course, Denmark is one the very most stable and prosperous countries in the world and thus an extreme case – nevertheless it indicates the direction of travel for other advanced economies.

For the Left this is wonderful news: the old constraints on borrow-and-spend policies look a whole lot weaker than they used to be. But those with more conservative economic instincts have their work cut out. They will need to persuade voters that the new normal does not mean a magic money tree for every garden. The example of Greece shows it is still possible to stretch the patience of one’s creditors too far.

Beyond that, there’s a perilous balancing act to pull off. On the one hand, to use our enhanced borrowing capacity to build our way out of the post-Covid slump; but on the other, to not allow cheap credit to fuel bad habits. The last thing we need now is public sector profligacy or private sector speculation.