February 22 2023 - 1:45pm

On May 6th 1997, then Chancellor of the Exchequer Gordon Brown sent a letter to the Governor of the Bank of England. In the letter Brown highlighted the New Labour manifesto commitment to “ensure that decision-making on monetary policy is more effective, open, accountable and free from short-term political manipulation”. In 1998, this new decision-making framework was brought into law under the Bank of England Act 1998.

These legal developments reflected broader changes in the discipline of economics. As inflation subsided in the 1990s, many attributed this new stability to central bank policy. It seemed that many central banks had cracked the code of setting interest rates to ensure healthy economic growth without disruptive price rises. Brown, and other politicians like him, believed that public policy could be set in line with economic science and so he gave free rein to the experts.

The experts really believed that they had cracked the code. In 1993 the monetary economist John B. Taylor published a paper with an equation that many assumed allowed central banks to set policy along scientific lines. The equation became known as the ‘Taylor Rule’. It measured the current rate of inflation and compared it to the economy’s potential for further growth. So, if inflation was high or the economy was running too hot, the rule advocated higher interest rates. If inflation was low or economic growth was sagging, it advocated lower rates.

While central bankers did not follow the Taylor Rule to the letter, it has nevertheless been a golden rule central bank policymaking since. That is, until recently. The chart below shows the Taylor Rule for the United States compared with the Federal Reserve’s interest rate. While the Federal Reserve’s interest rate has closely followed the Taylor Rule most of the time since the start of 2021 the two have diverged sharply.

Why is this? For the most part it is because we are seeing a combination of sluggish economic growth and high inflation. That means that the Taylor Rule is telling central bankers to raise interest rates sharply, but the central bankers are looking at the poor economic growth and are reluctant to raise rates. They are also eyeing up the overextended financial markets worrying that if they raise rates the speculative excesses that have been encouraged by low interest rates will collapse.

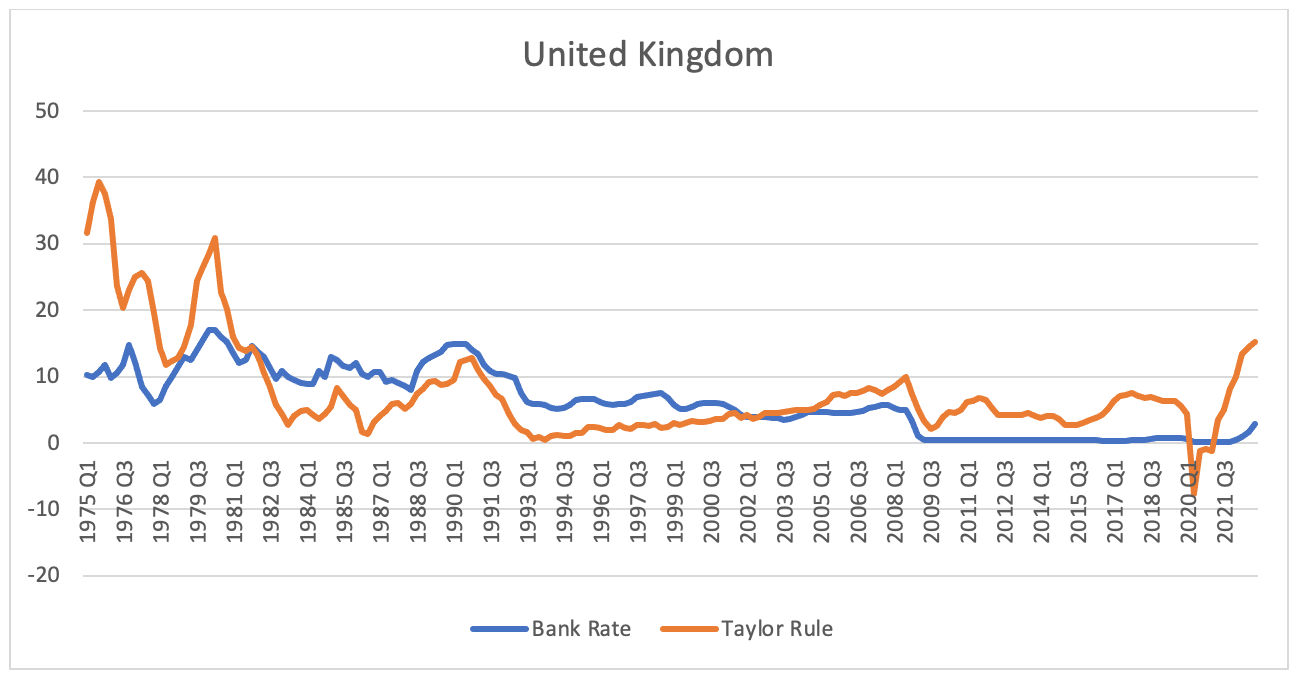

What about in Britain? As the chart below shows, the Taylor Rule has never worked as well in Britain as in the United States. There are a lot of reasons for this, but perhaps the primary one is that during this time the British economy has been in a state of decline. This decline has meant that inflationary pressures have been much more persistent in Britain than in the United States. Policymakers have therefore sought to moderate their use of using interest rate policy to steer the economy and instead have used it to promote financial stability and especially stability of sterling.

Nevertheless, as in the United States, since the start of 2021 the Taylor Rule has been screaming for the Bank of England to raise rates, but the bank has refused. If British central bankers followed the Rule, we would current have interest rates of over 15% rather than the 4% rates we currently see. So, as in the United States, central bankers are seeing a failure of their ‘scientific’ methods for setting interest rates in the face of economic dysfunction and stagnation.

Where does this leave us? Unless something changes soon, it looks like the Taylor Rule is heading for the dustbin of history. Unless the inflation and stagnation rapidly subsides — in which case economists can chalk this unusual period up to a blip — the scientific pretensions of central bankers will no longer be very convincing. In that case, we will be entering a world of monetary policy uncertainty.

Philip Pilkington is a macroeconomist and investment professional, and the author of The Reformation in Economics

philippilk

philippilk