Graphic by Krieg Barrie

How long do you imagine it takes someone to save to get on the property ladder? Five years? A decade? Until they’re in their thirties? Their forties, perhaps?

According to one recent survey, a waiter who squirrelled away a tenth of their salary would take over a century before they had accumulated enough to put down a deposit on an average first time property [1. Survey by HouseSimple, quoted in the Telegraph 10th June 2017] . Without any help from mum and dad, the average cook would have to save for 94 years. A receptionist, 85 years.

Surveys such as this highlight the way in which home ownership has become a distant dream for millions of people in Britain. It also tells us something about the real nature of economic inequality in many Western countries today.

Economic inequality

Mention economic inequality, and people usually think in terms of income inequality; the difference in pay between, say bankers on one hand, and waiters, cooks, receptionists and other workers on the other.

But that kind of income inequality in Britain is actually at a thirty-year low. The Gini coefficient – statisticians’ wonky way of measuring income inequality – shows that income inequality is falling in Britain [2. Office of National Statistics data, July 2017]. In fact, in many Western states the big increases in income inequality happened a generation ago – and income inequality has since slowed or even, as in the case in the UK, gone into reverse [3. For example, in Australia and other Western states income inequality is also declining. See John Slater from The Spectator; “Up the pointy end“] .

The problem in most Western states is not inequality of income – the gap between what waiters earn relative to bankers. Rather it’s the gap between what millions of other ordinary workers – such as waiters, cooks or receptionists – earn, and the soaring value of assets, whether those assets are houses or hedge funds [4. Office of National Statistics, Statistical Bulletin, Housing affordability in England and Wales: 1997 to 2016].

You don’t have to listen to a discussion about economic inequality for very long before someone mentions globalisation. But economic distress in the West is caused less by the new-found productivity of Chinese or Mexican workers. Cheap consumer imports have lowered the cost of living for Western workers [5. See HumanProgress.org for more detail, for example on the declining cost of groceries]. Asset prices have not increased compared to ordinary incomes because of globalisation, or foreigners – but thanks to our own central bankers.

The easy-money orthodoxy

For at least the past twenty-five years, central bankers in Britain, America, Japan and much of Europe have kept interest rates low and credit cheap. The effect of this has been to raise asset prices, with everything from houses to hedge funds rising in price relative to labour.

Its difficult to say when precisely this easy money orthodoxy took hold amongst Western policymakers. In Britain, it was sometime after September 1992, when we crashed out of the EU’s Exchange Rate Mechanism. While the UK had been members, policymakers had been prepared to raise interest rates to eye-watering levels in an attempt to ensure that Sterling closely shadowed the German Deutschemark at a particular rate.

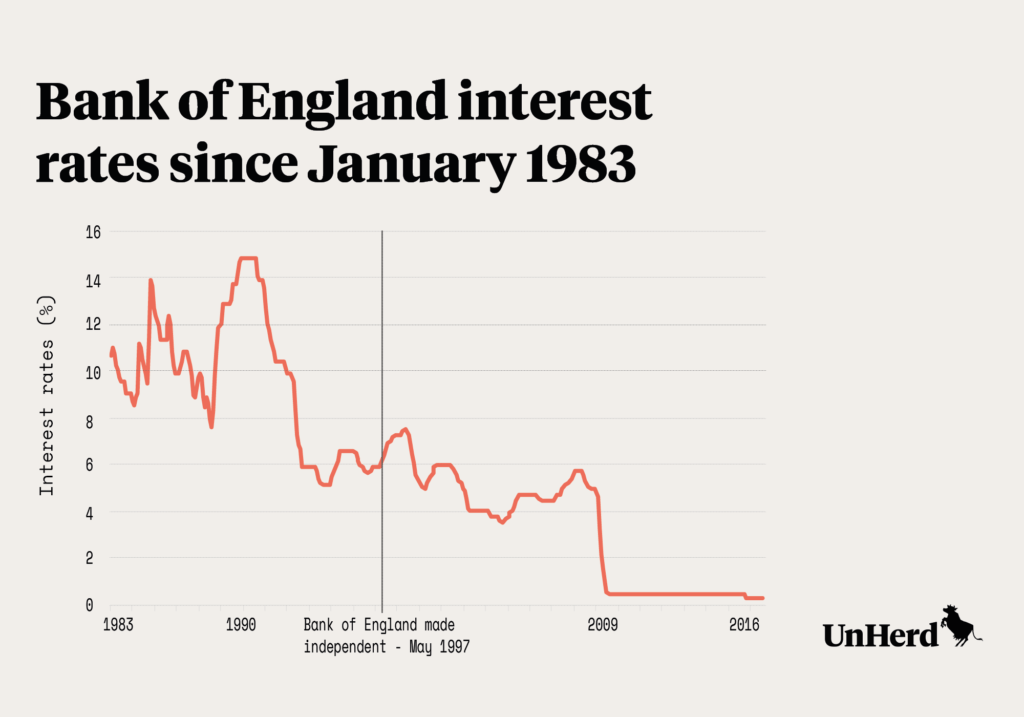

The low interest rate orthodoxy has dominated for almost all of the period since 1997 – when the Bank of England was made independent by then Chancellor Gordon Brown. This is hugely ironic given that central bankers were granted autonomy because it was feared politicians would use it to offer easy money as an inducement to the electorate to borrow and spend. Independent central bankers, as you can see from the graph below, have presided over a far looser monetary policy than the politicians ever managed.

Of course, this easy-money orthodoxy didn’t just take hold in Britain. Other countries started it even earlier. Japanese monetary authorities cut interest rates aggressively from the early 1990s, and have had near negative rates ever since.

The US Federal Reserve has had a policy of cutting or holding down interest rates in the face of almost any perceived threat to output;

- the 1987 stock market panic known as Black Monday;

- the Mexican crisis of 1994;

- the collapse of Long Term Capital Management in 1998;

- the Asian and Russian financial crises of the late 1990s;

- the dot com bubble;

- the September 11th terror attacks…

After the 2007 financial crisis, when the threat of falling output was all too real, rates were cut (to effectively zero) in many Western states. Unable to ensure more easy-money by lowering the price of credit, central banks began to buy up gilts, Quantitative Easing (QE), giving banks room to lend [6. Quantitative Easing means central banks and corporate banks do a swap; rental banks give corporate banks new money in return for financial assets. Corporate banks give central banks financial assets in return for that new money – which means they have more of it to lend out. Exchanging billions of pounds of bank assets for this new money has increased the ability of banks by billions to lend – as well has pushing up the price of those assets giving banks room to lend] .

Far from causing Western policy makers to seriously question their easy-money orthodoxy, that has prevailed over the decade since the financial crisis, they have doubled down on it. Why?

The economic consequences of central bankers

In the 1960s and 70s, Western economic policy makers believe that they could and should steer economic growth – and avoid nasty downturns – by spending more. The current crop of policy makers believe that they can use monetary stimulus in much the same way. Easy money raises output, they say. And for the past two decades, central bankers have been lauded as the omnipotent gurus, able to conjure credit and growth from no where.

Of course, those old fashioned Keynesians from yesteryear, we now know, never proved quite as good at cutting spending during an upturn as they were at increasing it in a downturn. So, too, today those who advocate monetary stimulus have proved good at hosing the economy with cheap credit. They have been less good at finding the right time to raise interest rates and unwind QE.

The kind of critical questions that ought to have been asked have seldom been considered by politicians and financial journalists. Yet it is becoming increasingly clear that there are downsides to easymoney economics.

The haves have got richer for simply having [7. In many parts of London, for example, someone who bought an average house in 1997 would have earned more for simply owning the deeds of that house than they would have done if they had earned the average income over the intervening years]. With the cost of borrowing so low, there has been an incentive to take out loans and invest the money in assets – the value of which would rise faster than the interest on the loan. This has been the basic business model from big time hedge funds to buy-to-let investors.

More credit means more debt. UK household debt is higher now in relation to income than at almost any point since the Second World War [8. See speech by Bank of England’s Alex Brazier, “Debt strikes back or return of the regulator?”. July 24th 2017 and Bank of England’s website for more detail]. Recent Bank of England figures show 140,000 people taken out home loans of more than 4.5 times their income over past year – a sharp rise on previous year [9. Bank of England report.].

Easy money economics means less incentive to save. Official data shows the savings ratio in the UK has fallen to 1.7% in early 2017 – the lowest rate since records began in the 1960s [10. The Daily Telegraph, 30 June 2017] .

Excess credit encourages excess consumption. It’s perhaps not a coincidence that Western states with the most relaxed monetary policy, such as Britain and America, have had the biggest trade deficits, importing more than they export.

With the price of credit set low, it has been harder for businesses and entrepreneurs to assess risk. Too many things look like a good bet and as a consequence a lot of bad investment decisions have been made – which will become evident when rates rise.

According to some estimates, 9% of non-financial firms in Europe are so-called zombie firms [11. CNBC report, 25 July 2017: “The plethora of monetary support in Europe over the last 5 years has allowed companies with weak profitability to continue to refinance their debt and stave off defaults”] – able to service the debt at low interest rates, but unable to pay it back. As the OECD has pointed out, these zombie firms – kept alive by low interest rates – help explain poor productivity performance and slow growth not just in Britain, but in America and much of Europe too [12. OECD paper, The Walking Dead? Zombie firms and productivity performance in OECD countries].

Easy money economics is also starting to produce political consequences. With little prospect of getting on to the property ladder, millions of young voters in Britain – including no doubt plenty of waiters, cooks and other ordinary workers – are drawn to the radicalism of Jeremy Corbyn’s Labour party. Corbyn’s economic platform, often dismissed as simply old fashioned socialism, can also be seen as an effort to address some of the imbalances and injustices caused by our central bankers. Instead of QE, for example, the Corbynistas want People’s QE – a kind of massive fiscal and monetary stimulus rolled into one. Their answer to rising house prices is to toy with the idea of rent controls.

These left-wing interventions might only deal with some of the symptoms of monetary mismanagement. But unless we want them to become public policy, we need to find an alternative.

THE ALTERNATIVES?

1.Higher interest rates

The price of credit is going to have to go up, whether policymakers choose to put interest rates up or not. Why? Because prices cannot be fixed forever – and artificially low interest rates are a form of price fixing. There will come a time – sooner or later – when Western governments discover the they need to raise interest rates in order to borrow.

Of course, even a modest increase in interest rates would mean tens of thousands of households going bankrupt in Britain, as the UK Insolvency Service has pointed out. Firms across Europe and the US would cut payrolls. Unemployment would rise. The pain and disruption will be enormous. But we are going to enter a world of least worst options, and easy-money is not going to be sustainable forever. And it won’t be all bad news…

A rise in rates would mean a fall in house prices. Middle England and America might howl but housing would become more affordable for millions, not least workers of modest means.

The massive transfer of wealth to those with houses or hedge funds or any other kind of asset from those without, would end. It might even go into reverse. Good.

Thousands of zombie firms would be killed off. The bout of creative destruction [13. The term “creative destruction” was coined by the economist, Joseph Schumpeter. It refers to the way in which innovation and change within capitalist systems involves finding new ways to organise finite resources. That creative process necessarily means disrupting some of the older established ways of ordering resources – which is destructive. In this context, the resources currently tied up with zombie firms, unable to expand and innovate, would be reallocated to new firms that were not so mired in debt, and could not only serve their current customer base, but expand and innovate.] that would follow a rate rise would see lots of immediate destruction – but the creative bit would eventually follow and productivity would finally rise.

2. Accountability for central bankers

It is rare that a central banker ever seems to get the sack [14. Charlotte Hogg, Chief Operating Officer at the Bank of England was forced out in March 2017. Why? She apparently failed to declare that she had a brother working at a big corporate bank. Failure to comply with such bureaucratic requirements is seen to be seen as a resigning offence. Setting interest rates recklessly low, or allowing the reckless accumulation of debt in the wider economy does not.]. This is not because they never make mistakes (see the financial crisis of 2007 for details). It’s because central banker independence has come to mean an almost complete lack of accountability.

Congress and Parliament need to assert oversight over those that make key economic decisions which affect us all. Somehow the European Central Bank needs to be made answerable for how it runs the Euro, too.

If central bankers were properly answerable, politicians, financial journalists and commentators might at last begin to ask the kind of questions about monetary policy that are long due. The fact that they have failed to do so is not a case of conspiracy (these aren’t the kind of people competent enough for that), but complacency and group think. When it comes to reporting on financial matters, the mainstream media too often resorts to cliché (see the BBC coverage of the financial crisis over the past decade for details).

3. Government debt – turning off the taps

If the mainstream media was up to the task of informing and educating us, they would alight on the fact that easy money economics isn’t really about giving the people cheap mortgages and credit. It happens, fundamentally, because it suits big government.

Governments, you see, like to borrow and spend beyond what they take in tax. Rather than just rely on this year’s tax revenue, governments issue bonds; IOUs in return for ready cash. Easy money economics makes it easier to borrow this way. In order to normalise monetary policy, we must stop it serving big governments’ fiscal appetites. As debt becomes more expensive, governments will have to accumulate less debt.

4. Radical bank reform

Government isn’t the only vested interest that favours easy money. Big banks do rather well out of it, too. (And, of course, with so many central bankers having a background in corporate banking, why wouldn’t they assume that easy-money economics is a Good Thing? For their former – and possibly future – employers, it is).

For as long as corporate banks are able to conjure almost unlimited amounts of credit out of thin air, they will have a vested interest in easy-money economics. An end to this lax form of monetary policy will expose the way in which many big banks have been living off a form of state subsidy. All the more reason to start raising rates and unwinding QE.

Former MP for the Conservative Party and Ukip, Douglas Carswell was a leading campaigner for Brexit. In his latest book, ‘Rebel: How to Overthrow the Emerging Oligarchy’, he examines next steps for anti-establishment movements

DouglasCarswell

DouglasCarswell

Thank God for UnHerd and Freddie Sayers. You learn much more about COVID-19 from his interviews with experts than from any one of our Canadian networks. I can remember anyone making the point that Michael Levitt does that “R0 is a faulty number, as it is meaningless without the time infectious alongside.” Our federal and provincial governments have all pretty much gone the full lockdown route. On April 30 the Parliamentary Budget Officer revised his projection for real GDP decline in 2020 from 5.1% as of April 9 to 12.9%. This is an absolutely staggering loss. From peak to trough in the 2008-09 recession, the Canadian economy only suffered a 5.4% loss. And if Michael Levitt is correct, much of that loss will be unnecessary. We should have been taking better care of our residents in nursing homes and instituted a milder Swedish-style form of lockdown.