February 24 2023 - 6:00pm

Last week the Centre for Research on Energy and Clean Air (CREA) released a weekly snapshot of Russian fossil fuel exports. Since the price cap on Russian oil was announced in December 2022 and the snapshot provides data up until February 2023, it allows us to assess how effective sanctions against Russian crude oil have been.

Some have already pointed out that the sanctions have not actually stopped the European Union from buying Russian fossil fuel products. In fact, as of February the EU remains the second largest importer of Russian fossil fuels — trailing China, but still larger than India. But there is no doubt that there has still been an enormous shift: before the sanctions, the EU was by far the largest importer of Russian fossil fuels.

Yet the real question is not whether the EU has cut its imports of Russian fossil fuels. Much more relevant is whether the sanctions have impacted Russia’s ability to export its energy products. If the EU has been forced to starve itself of energy in spite of the continued robustness of Russian energy exports, then it is Europe — and the United Kingdom — that the sanctions are hurting, not Russia.

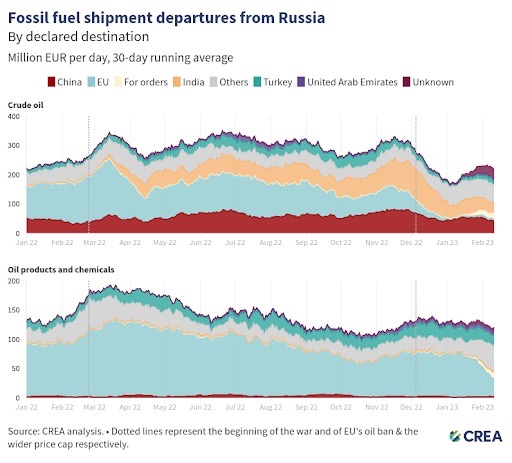

When we look at CREA’s chart on Russian oil exports, it does appear that they have fallen since the price cap. As we can see, following the imposition of the price cap last December Russian crude oil exports have fallen from over €300m per day to under €250m per day. Looked at in a broader context, however, this is not a particularly dramatic decline. Economists tend to compare exports in one year to exports in the same month the previous year. In February 2022, Russian oil exports sat at around €250m per day, not far off where they are this February.

But even this is misleading, because the price of Russian oil has declined. Since the start of December Urals oil has fallen from around $66 per barrel to roughly $53. Some have claimed that this is an effect of the energy price cap, but if we look at other oil markets this seems unlikely to be the main cause. Today the difference between the Russian Urals price and the European Brent price is around $32 per barrel. Yet in the wake of Russia’s invasion of Ukraine, long before the price cap was imposed, the difference was over $35 per barrel.

The decline in the Russian oil price is mostly being driven by an overall global decline in prices, which has come about because Western economies are slowing down and will likely face recession this year. When the economy sags, less fuel is needed and so its price falls.

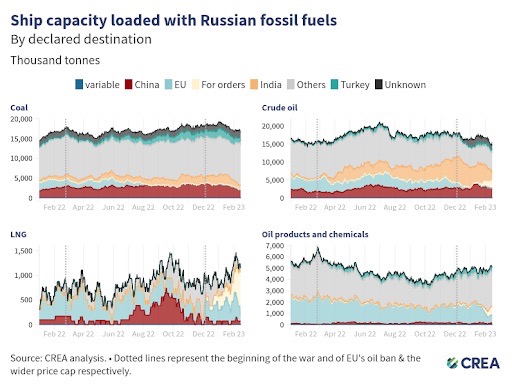

To control for this, the best indicator as to whether the energy price cap has damaged Russia’s ability to export its energy products is to look at the physical quantities of the exports. These can be seen in the chart below.

Here we see a different picture emerge, especially for crude oil. In February 2022 Russian crude oil exports stood at around 15 million tonnes per day. One year on, these exports have fallen slightly to 14 million tonnes — a fall which is hardly statistically significant and which may even be explained by the looming recession. There is no other way to interpret the data: the sanctions simply have not hurt Russia all that much. It has largely replaced its exports to Europe with exports to India and China, among others.

Meanwhile, Europe is being starved of energy. Despite the much-touted decline in gas futures prices, energy bills in Europe remain stubbornly high — no one except speculative traders pays the futures price, so serious analysts need to look at how much people are paying in their bills. In response to these high prices, gas consumption in Europe has fallen nearly 20%. Nor is this just impacting consumers: the European manufacturing sector has been contracting since the summer.

If the sanctions are designed with a goal to damage European economies and hurt European consumers, they have worked a treat. If, however, they have been designed to hobble Russia’s ability to export its energy products, they have been somewhat less successful.

Philip Pilkington is a macroeconomist and investment professional, and the author of The Reformation in Economics

philippilk

philippilk