December 13 2022 - 1:00pm

It’s cold outside. In the 10 years that I have lived here, I do not think I remember seeing so much snow coverage in London. The markets are feeling the cold too: over the weekend the energy markets recorded record prices. On Sunday, the price for power at peak time (5-6pm) for the following day hit £2,586 per megawatt-hour — a record. It appears that promises of a warm winter were greatly exaggerated.

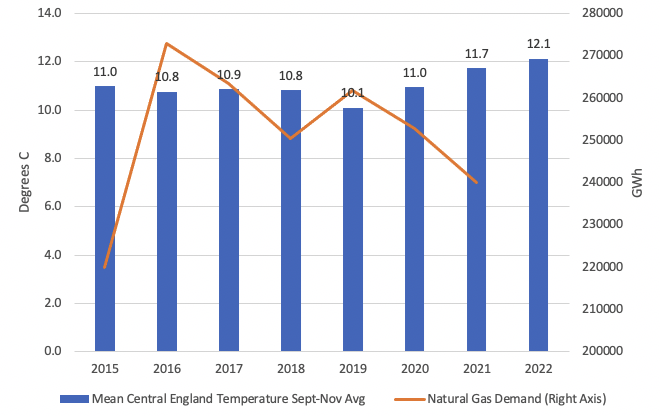

This is not surprising to anyone who studied the data for temperature and for winter gas demand. The first and most obvious thing to note is that warmer weather in the period September to November does not predict warmer weather in December. For example, in the years 2015-21 the warmest September to November period was recorded in 2021 (11.7°C), but this was followed by a very average December (6.3°C). Meanwhile, the warmest December in this period, recorded in 2015 (9.6°C), was preceded by a very average September-November period (11°C).

When natural gas demand is added into the mix, the waters only become more muddied. The chart below shows September-November average temperature by year together with gas demand in the fourth quarter.

While it is true that 2022 saw higher-than-average temperatures in this period, it was not that much higher than, say, 2021. Did we really expect a 0.4°C increase in autumn temperatures to save us from a major energy crisis? What’s more, there is clearly no reliable relationship between autumn temperatures and autumn-winter gas demand. Gas demand was lowest in autumn-winter 2015, yet seasonal temperatures were about average. Gas demand was highest in 2016 yet, once again, temperatures during that period were roughly average.

The other thing that stands out in the chart is that gas demand does not fluctuate all that much. The largest surge we saw in gas demand in this period (2016) was only around 8.5% higher than the period average, while the largest decline (2015) was only around 12.5% higher than average.

But now, with temperatures plunging, we are running out of road. How will politicians respond? Most likely, they will pull another rabbit out of the hat and blame the looming recession, telling us that the recession will reduce energy demand. This, too, does not stand up to scrutiny. During the last major recession (2008-09), GDP growth contracted 4.2% in Britain while gas demand only fell 6.7%. By contrast, in 2011, when the economy was humming along at 1.5% GDP growth, gas demand fell almost 17%. As with autumn temperatures, GDP growth is a bad predictor of gas demand.

At the end of the day, the energy crisis is a real crisis. It is not a crisis of perception. The simple fact is there is not enough gas. Either we figure out a way to get more or we substitute the gas for another energy source; otherwise, we are in a great deal of trouble.

Philip Pilkington is a macroeconomist and investment professional, and the author of The Reformation in Economics

philippilk

philippilk